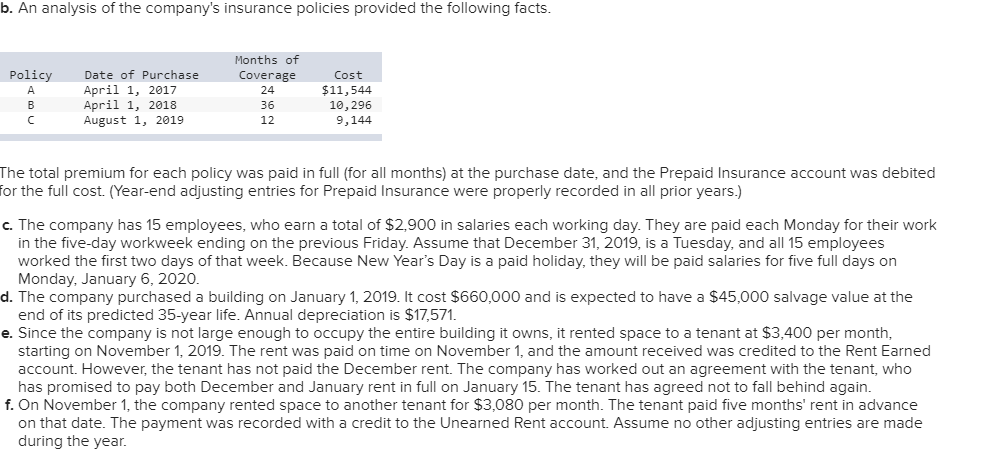

Good HUD home loan cost, otherwise MIP, was paid a-year, beginning from the closing for each and every 12 months of construction then annually.

An excellent HUD financial advanced, or MIP, are paid off per year, delivery at the closure for every year off design and then annually. MIP to possess HUD multifamily construction fund are:

To learn more about HUD multifamily build financing like the HUD 221(d)(4) financing, fill in the proper execution below and you may an excellent HUD financing professional will get in touch.

What’s the reason for MIP (Mortgage Advanced)?

The goal of MIP (Home loan Advanced) is to provide most shelter into financial in the eventuality of default on the financing. MIP is actually an annual percentage on an excellent HUD home loan, repaid during the closure and you may a-year. To have HUD 223(f) funds, MIP is actually twenty five foundation situations to have properties playing with an eco-friendly MIP Protection, 65 base things for market price features, 45 basis circumstances for Area 8 otherwise the fresh currency LIHTC services, and you can 70 foundation affairs having Section 220 urban revival systems you to commonly Part 8 or LIHTC. To possess HUD 232 finance, MIP try step one% of loan amount (due during the closing) and you may 0.65% a-year (escrowed month-to-month).

MIP (Mortgage Top) costs vary according to the mortgage system. To the HUD 223(a)(7) loan program, MIP prices are 0.50% initial and you can 0.50% annually to possess market speed functions, 0.35% upfront and you may 0.35% a-year getting sensible characteristics, and you will 0.25% initial and you may 0.25% annually having Environmentally friendly MIP properties. Into the HUD 221(d)(4) mortgage program, MIP prices are 0.65% initial and you may 0.65% a year getting field price characteristics, 0.45% initial and you may 0.45% annually to own sensible characteristics, 0.70% initial and you can 0.70% per year for Part 220 functions, and 0.25% upfront and 0.25% a year for Green MIP features. Toward HUD 223(f) loan program, MIP costs are twenty five basis factors getting qualities using an eco-friendly MIP Avoidance, 65 basis issues to possess industry rate properties, 45 foundation things getting Part 8 otherwise this new money LIHTC functions, and 70 basis circumstances to online payday loans West Virginia own Point 220 metropolitan restoration systems you to definitely aren’t Part 8 or LIHTC. To find out more, delight see just what was MIP (Home loan Premium) and MIP (Financial Cost) while the HUD 223(f) Loan Program.

What are the advantages of MIP (Financial Premium)?

MIP (Financial Advanced) is a vital consideration when examining HUD fund. It is a form of insurance rates you to protects the lending company out of losings you to definitely occur whenever a debtor non-payments. When you’re upfront and you can annual MIPs was costs you must view when investigating your loan possibilities, there are ways to remove them – plus instead a decrease, HUD fund will always be basically much less costly than many other types away from multifamily financial obligation, also Federal national mortgage association and you will Freddie Mac computer fund.

- Defense towards the lender of loss one occur whenever a borrower non-payments

- Smaller charges for HUD loans versus other kinds of multifamily personal debt

- The capability to treat MIPs from Eco-friendly MIP Avoidance program

Just how long do MIP (Home loan Premium) history?

MIP (Home loan Premium) lasts for living of your mortgage, in fact it is set from the a fixed speed. not, just like the a debtor takes care of the main harmony of its mortgage, the level of MIP these are generally required to pay refuses as well. This information is considering HUD 221(d)(4) Loans.

Which are the differences between MIP (Financial Premium) and PMI (Private Mortgage Insurance coverage)?

MIP (Home loan Insurance premium) and you will PMI (Private Mortgage Insurance rates) was both brand of financial insurance rates you to manage lenders regarding the experiences out-of a debtor defaulting on their mortgage. MIP is typically you’ll need for funds supported by the new Government Homes Administration (FHA), if you find yourself PMI is usually you’ll need for loans perhaps not backed by the new FHA.